By Doug Payne

.jpg) From SolarTech’s perspective, we are reaching points in the U.S. solar market in general and California specifically where market inflection points are now gated by process related balance of system (Process BoS). These costs are characterized as building the business case, design/engineering, finance contracts, permitting, inspection and O&M. We see a number of challenges associated with what we term ‘soft or hidden’ costs. As a result of the need to transit smoothly from a policy-driven market to a self-sustaining consumer driven market, we are driving several solutions to these issues in the areas of workforce, performance, finance, and permitting. We want to implement business systems to increase our industry’s overall capacity to deliver PV across the entire value chain by a minimum of 20% annually over the next 5 years. From SolarTech’s perspective, we are reaching points in the U.S. solar market in general and California specifically where market inflection points are now gated by process related balance of system (Process BoS). These costs are characterized as building the business case, design/engineering, finance contracts, permitting, inspection and O&M. We see a number of challenges associated with what we term ‘soft or hidden’ costs. As a result of the need to transit smoothly from a policy-driven market to a self-sustaining consumer driven market, we are driving several solutions to these issues in the areas of workforce, performance, finance, and permitting. We want to implement business systems to increase our industry’s overall capacity to deliver PV across the entire value chain by a minimum of 20% annually over the next 5 years.

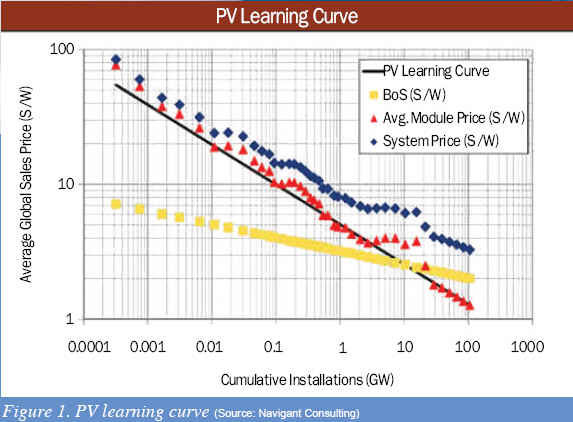

What is abundantly clear at this point is the balance of system/process costs is mission critical according to PV Learning Curves from Navigant Consulting. Unless we ‘learn faster’ we risk growth stagnation, or at a minimum, have asymptotic consumer price curve reductions until breakthrough improvements are made in BoS and Process costs.

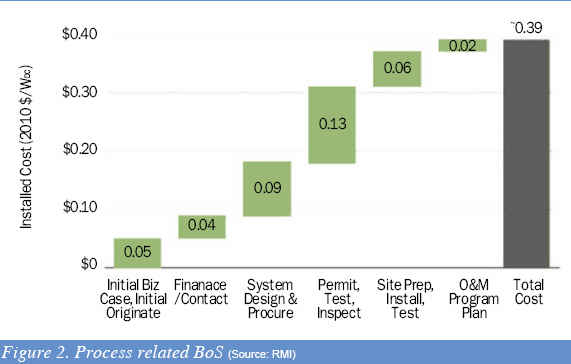

According to finding at Rocky Mountain Institute’s recent June 2010 Process Charrette, Process related BoS and Project delays account for up to US$0.39/ Wp at least, causing delays in building the business case, lost execution, and lost kWh production of the systems themselves.

In addition, execution of both residential and non-residential PV projects remains a barrier to growth. As indicated by the most recent CSI program annex data, the average time from rebate reservation date to approval of the incentive claim form dwarfs the actual project construction time, especially with respect to residential systems. Specifically, average residential project timelines between these two milestones are currently 97 days compared to only 3-5 days on site for the average 4-5 kW system. Non-residential is longer at 216 days for obvious reasons due to the increased complexity or the projects. The comparison of non-residential timelines to on-site time is more challenging because of the variety of factors. In either case, removing these delays with market-based solutions is the focus of SolarTech’s work.

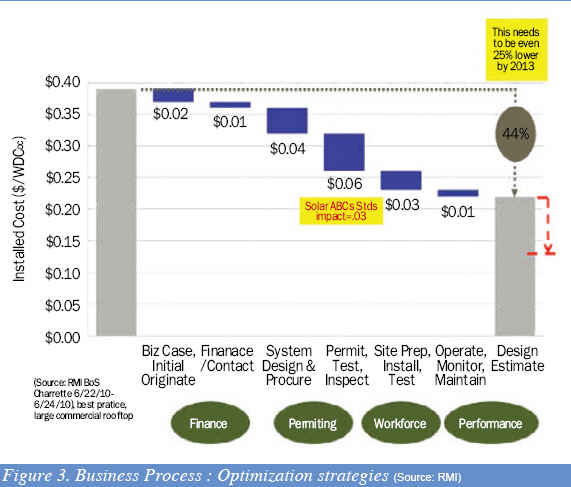

To do this, we are taking an integrated approach from manufacturing, design/engineering, installation, project finance, cities, utilities, test /certification, and workforce development organizations to achieve a Process BoS cost reduction roadmap (see Figure 3).

Taking each in turn, the workforce goal is to integrate industry, public, private work-force training to create value-chain-wide job training road-map by 2010. This will address common problems such as shortfalls in strategic, comprehensive industry approa-ches combined with competency models, career ladders, and specialties in various regional programs. The goal is to reduce hiring costs, times by 20%-30% through several completed or ongoing initiatives: multi-year, multi-phase, multi-discipline integrated programs go beyond the roof with training programs. Green Innovation Grant through 2012, a framework for workforce development, was a kind of a workforce acceleration methodology.

Turning to finance, the goal is to achieve ‘bankable’ projects, providing better due diligence tools for project developers and achieving a 25% reduction in transaction costs and/or time. We are addressing common problems such as the relatively newness and significant complexity of ‘finance products’, the lack of standardization and transparency in financial and contractual terms which lead to wasted time negotiating all language as opposed to focusing on ~20% variation deal to deal. We have been or are in the process of developing solutions such as a Standard PPA Commercial Project Contract, PPA Site License Agreement, Standard Due Diligence Checklist, Standard Request for Information and Consumer Guide of Financing Options. We see a future state to solidify confidence in solar financing, enable standard processes to reduce risk, thus increasing the probability of capital flowing to high quality, predictable projects.

Our performance work is tightly tied to the finance efforts. The goal is to achieve 25% faster buying decisions through standard performance metrics, energy production tools. We are attempting to address common problems such as lack of standard language, metrics, and tools for PV system performance and inconsistent economics impact the value proposition to consumers. Broad reliability data, FMEA, MTBF, MTTR, etc., is in its infancy, and industry system uptime and availability <90% (market expectation). We see the following standards at all levels as essential in this area. This ranges from terminology, monitoring, design degradation to LCOE calculations, bankable performance ratios, guaranteed outputs, and 3rd party certification. Ultimately, the end product is to arrive at a Good Faith Estimate tool, coordinate at system commissioning with system monitoring and data interoperability standards developed in close partnership with the SunSpec Alliance (www.sunspec.org). We see a future state of demystifying energy (kWh) versus power (W) for consumers through widespread education supported by unified 3rd party performance standards backed by ensuring 90% of systems achieve 90% uptime or better over time. This will establish tighter linkages between energy ratings, power ratings and project finance. Our performance work is tightly tied to the finance efforts. The goal is to achieve 25% faster buying decisions through standard performance metrics, energy production tools. We are attempting to address common problems such as lack of standard language, metrics, and tools for PV system performance and inconsistent economics impact the value proposition to consumers. Broad reliability data, FMEA, MTBF, MTTR, etc., is in its infancy, and industry system uptime and availability <90% (market expectation). We see the following standards at all levels as essential in this area. This ranges from terminology, monitoring, design degradation to LCOE calculations, bankable performance ratios, guaranteed outputs, and 3rd party certification. Ultimately, the end product is to arrive at a Good Faith Estimate tool, coordinate at system commissioning with system monitoring and data interoperability standards developed in close partnership with the SunSpec Alliance (www.sunspec.org). We see a future state of demystifying energy (kWh) versus power (W) for consumers through widespread education supported by unified 3rd party performance standards backed by ensuring 90% of systems achieve 90% uptime or better over time. This will establish tighter linkages between energy ratings, power ratings and project finance.

Finally, we turn to permitting?everyone’s favorite topic. Our goals are to reduce permit time by 50% by 2011 for both residential and commercial systems, primarily in distributed generation market sectors. Common problems are significant variation by jurisdiction, which leads to a lack of consistency, transparency, predictability creating high overhead for contractors, integrators and project developments. In terms of solutions, it is time for a ‘step change’ in driving down BoS costs. We need to create consistent business systems, training, apply technology & SW as appropriate through a multi-Level, multi-phased strategy relative to local market conditions. We envision a future state of integrated, online processes and tools cut costs and delays 50-70%. We feel the need to integrate the permitting, inspection, interconnection processes or at least the functions in some fashion similar to how municipal cities/utility structures are able to collapse business operations.

In summary, at least with respect to the California market which we’re most familiar with, it is now all about Process BoS cost reduction. Taken together, we believe our programs to remove 50% of the paperwork, 40% of delays, reduce BoS, soft costs 60-70% can contribute a US$0.02/ kWh cost reduction to the overall PV system cost learning curve, accelerating US$ millions in market opportunity. Our strategy is to implement best practices in California through 2011/2012, validate, and scale.

Stepping back and building on our work in California, what this provides to the industry is a path from policy-driven markets to a self-sustaining market. In order to do this, we have recently partnered with Carbon War Room to provide recommendations for multiple operational pathways to accelerate market-based industry-led solar industry transformation to a low carbon economy. These pathways will address several barriers:

Top Barriers to Accelerated Market Growth

-Lack of cohesive data for site information, utility rates, local codes, and geographical conditions

-Insufficient product standards at the module, inverter, racking, and balance of system level

-Inadequate harmonization of codes and complex and expensive permitting procedures

-A lack of flexible, consistent, and proven financing mechanisms

Operational Pathway to Achieve Substantial Emissions Reduction by 2020

1. Harmonization of solar specific codes at the local level across all states

2. Open architecture to allow seamless flow project information through the entire life cycle

3. Uniform B2B ie. SolarTech certified and B2C ‘Strategic Solar Score’ credit system

4. Targeted campaign linking Consumer opportunity with economically viable sites at local levels

5. Optimized supply chain from order through net meeting--Just in Time

These pathways are informed by several guiding principles for systems integration, business practices, leveraging information technology, and accelerating time to market for new products.

Data Integrity

Economic feasibility of a roof- or ground mount solar site is determined from fractured data across various public and private organizations, with no simple way to aggregate and verify site characteristics. This lack of cohesive data breeds uncertainty in a PV transaction. Mitigation requires a customized evaluation of each site, breeding distrust among potential customers, financiers, and regulatory bodies about the viability of any given solar power development project. Consumers need non-technical information and consistent data on proposed solar systems to make better informed, faster, lower risk buying decisions. The industry must harmonize key data elements of predictive modeling to meet the consumer needs for clear choices to buy based on US$/kWh energy ratings rather than power ratings on a site by site basis.

Efficiency Everywhere

Solar business processes span organizations, industries, and sectors; reducing system cost resulting from business process inefficiencies doesn’t fall within most traditional job descriptions or organizational charters. Installing a Distributed Generation (DG) PV system involves many steps. Overall time requirements can range from 22 weeks for a best-case small, residential system to 50 weeks for a worst-case large, commercial system. Retail prices for DG systems will be held artificially high while consumers bear the costs of slow private/public business process improvements. No one has been able to harness market forces to drive voluntary efficiency improvement by key stakeholders. For example, all solar projects require local jurisdiction approval to ensure public safety and construction code compliance. The complexities increase when new products and construction techniques are introduced into the market creating the need to update, or revise existing permitting procedures ill equipped to handle the rapidly changing PV industry. Currently, little motivation exists at the local level to harmonize the 3000+ local solar markets aka Cities.

Projects Vs. Transactions

Financing for both residential and commercial markets is increasingly complex, resulting in longer sales cycles necessary to gain consumer confidence prior to closing a transaction, in addition to protracted legal reviews and associated fees. Lowering transaction barriers frees up markets and enables new participants to come. Standardized transaction instruments, consumer educational workshops and materials are essential. DG Solar project contracts need to be ubiquitous, much like rental-car or auto-purchase contracts.

Opportunities to Accelerate Deployment of Clean-tech Solutions

Robust Product Pipelines are essential given the inherent commercialization barriers in the solar value chain due to the various private/public stakeholders. Partnerships of unprecedented scale and complexity must be created along with commercialization methodologies having defined phases from initial concept through product launch, representing increasing levels of investment while lowering risk. We see clearly defined entry and exit requirements, with visibility into each phase entry and exit requirements. This creates a structured framework to move products to markets.

Enabling tools would follow in the way of software, documents, templates and education to create visibility, removing barriers to information flow, and identifying viable technologies sooner. This would result in more viable products, faster time to market, higher quality while less viable products terminated earlier, reducing investment risk.

In closing, SolarTech has always been about collaboration across multiple stakeholders to find solutions to issues of common concern. We’re always had an eye towards systematic standardization across public/private/non-profit business systems as the fundamental end game to achieve the economies of scale so critical to moving solar energy towards displacing carbon-based energy sources. We believe we have correctly identified the core issues in our areas of focus, proposed specific actionable solutions, and amassed significant industry, NGO, government, and other partners to drive development and adoption of market-based solutions to reduce solar industry costs. Through these efforts, we look forward to a day when Solar Just Happens. Everywhere.

Doug Payne is Co-founder and Executive Director of SolarTech (www. solartech.org). Prior to being appointed as SolarTech’s first Executive Director, Payne led the Commercial Business Development Division of Real Goods Solar, serving northern and central California.

Payne has nearly 20 years of engineering, program, and business management experience. Payne’s solar inspiration came 20 years ago as a member of Canada’s inaugural entry in the 1990 World Solar Challenge, a solar car race across Australia. He holds a BS degree in Mechanical Engineering from Queen‘s University, Ontario, Canada.

For more information, please send your e-mails to pved@infothe.com.

ⓒ2010 www.interpv.net All rights reserved. |

.jpg)